Emerging risk

Carpe Cyber

Cyber risk intelligence for carriers moving beyond traditional signals.

Primary buyer: Innovation, underwriting, and risk leadership

Related workflow: Emerging risk and cyber

Extend the same intelligence model into cyber and adjacent risk.

Overview

Carpe Cyber expands the platform into cyber and emerging risk, applying the same disciplined intelligence model to the categories carriers increasingly need to understand.

Carriers do not want a disconnected emerging-risk experiment. They want a believable extension of a trusted intelligence model.

Buyer and team

Innovation, underwriting, and risk leadership

Workflow problem

Why teams buy this.

Carriers need adjacent risk intelligence, but disconnected tools are hard to sponsor and even harder to trust.

Inputs and outputs

What the product looks at and what teams get back.

Inputs and signal sources

Outputs and deliverables

Data usage

What this product uses and what it does not.

Clear guardrails on data usage help teams evaluate fit, trust, and compliance readiness.

Data we use

Data we do not use

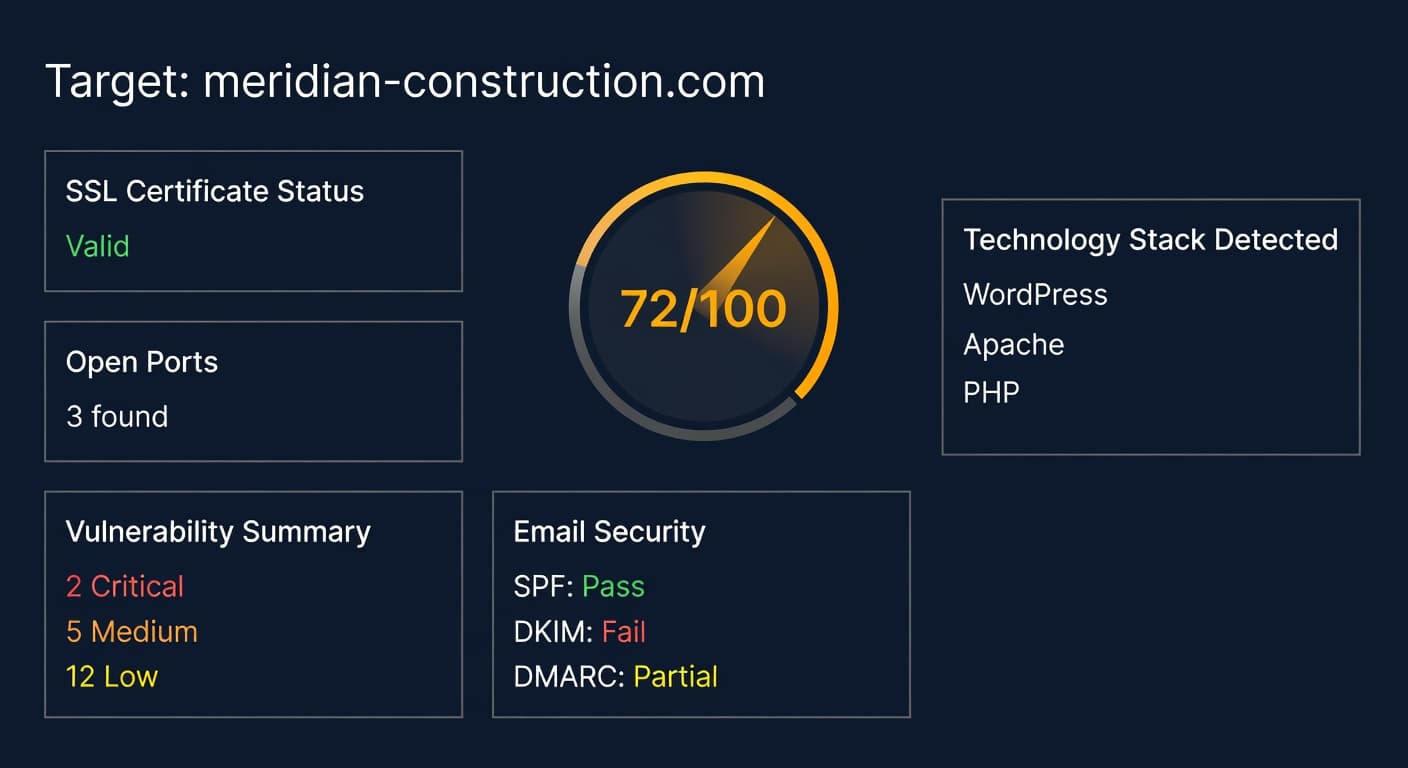

How it works in practice

The product in action.

See the product in context — how it captures signal, organizes findings, and delivers output into the workflow.

Cyber risk signals are assessed and organized for underwriting and emerging-risk operating reviews.

Operating motion

How it works in practice.

Implementation

Implementation path and requirements.

6 weeks for pilot deployment, then phased expansion by category.

Steps

Requirements

Why buyers trust it

Built for reviewable output and real workflow fit.

Enterprise buyers care about signal quality, output clarity, and whether the product fits how teams already make decisions.

Keeps the same signal-to-workflow discipline as core Carpe products

Feels like an extension, not a separate experiment

Supports platform expansion without fragmenting the buyer story

Expansion path

Related products and the next logical motion.

This product sits inside the broader emerging risk and cyber story and can expand into adjacent workflows cleanly.

Expansion path

FAQ

Questions teams ask before rollout.

Answers on data sources, implementation, pricing model, integration, and compliance.

What data does Carpe Cyber use?

Carpe Cyber uses external cyber-relevant signals and carrier-defined exposure context to generate prioritized, reviewable findings.

How quickly can a pilot be launched?

Most carriers can run an initial pilot in about 6 weeks, then scale to more exposure categories as governance matures.

How is pricing typically structured?

Pricing is generally aligned to exposure scope, portfolio coverage, and reporting depth needed for underwriting and innovation teams.

Can this integrate with underwriting and risk workflows?

Yes. Outputs are designed to fit existing underwriting and emerging-risk operating reviews rather than creating a parallel workflow.

How do you support compliance and control?

The product emphasizes reviewable output, defined scope, and governance-aligned deployment for enterprise use.

See this product in a live workflow walkthrough.

Carpe can tailor the conversation around the buyer, the operating problem, and the adjacent products that matter most for adoption.